Note: if the terms “interconnection queue”, “ISO”, or “RTO” are confusing to you, read our 1-min primer/FAQ here first

We used Interconnection.fyi‘s daily-updated dataset to analyze the state of the interconnection queues this month.

To be precise, we took a snapshot of the queue from Interconnection.fyi’s dataset at Jan 1, 2024 to produce these charts. Interconnection.fyi processes daily updates of the queue - for access to this historical data, or if you want any reports constructed of the data, contact us here.

Here are some trends we’ve found:

What’s in the queue right now?

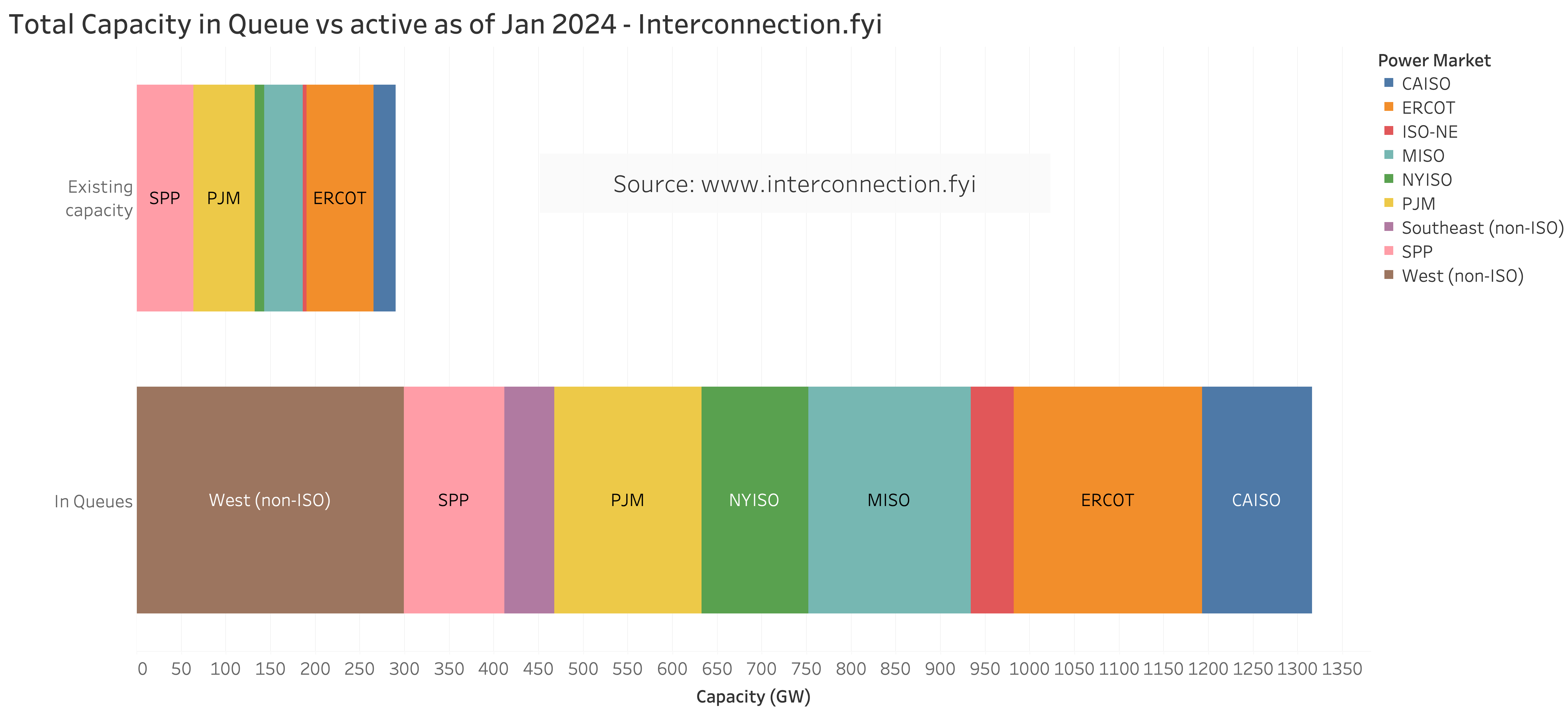

1.3 terawatts of capacity in the queue

Interconnection.fyi aggregates queue data across all 6 major RTOs/ISOs and 20 utilities in the U.S.

Based on this data there are currently at least 1.3 terawatts of capacity in the queue. 1.3 terawatts of capacity being planned. And that is not counting the long tail of utilities and other distributed energy assets Interconnection.fyi is not gathering presently in the US.

How much is 1.3 terawatts? Well there’s 300 GW (0.3 terawatt) in operation currently that have gone thru the queues listed above. 1.3 terawatts is 1,300 gigawatts, and 1 GW could power around 850,000 households at a given time.

Analysis of capacity in queues

Let’s look more into the in-queued capacity data

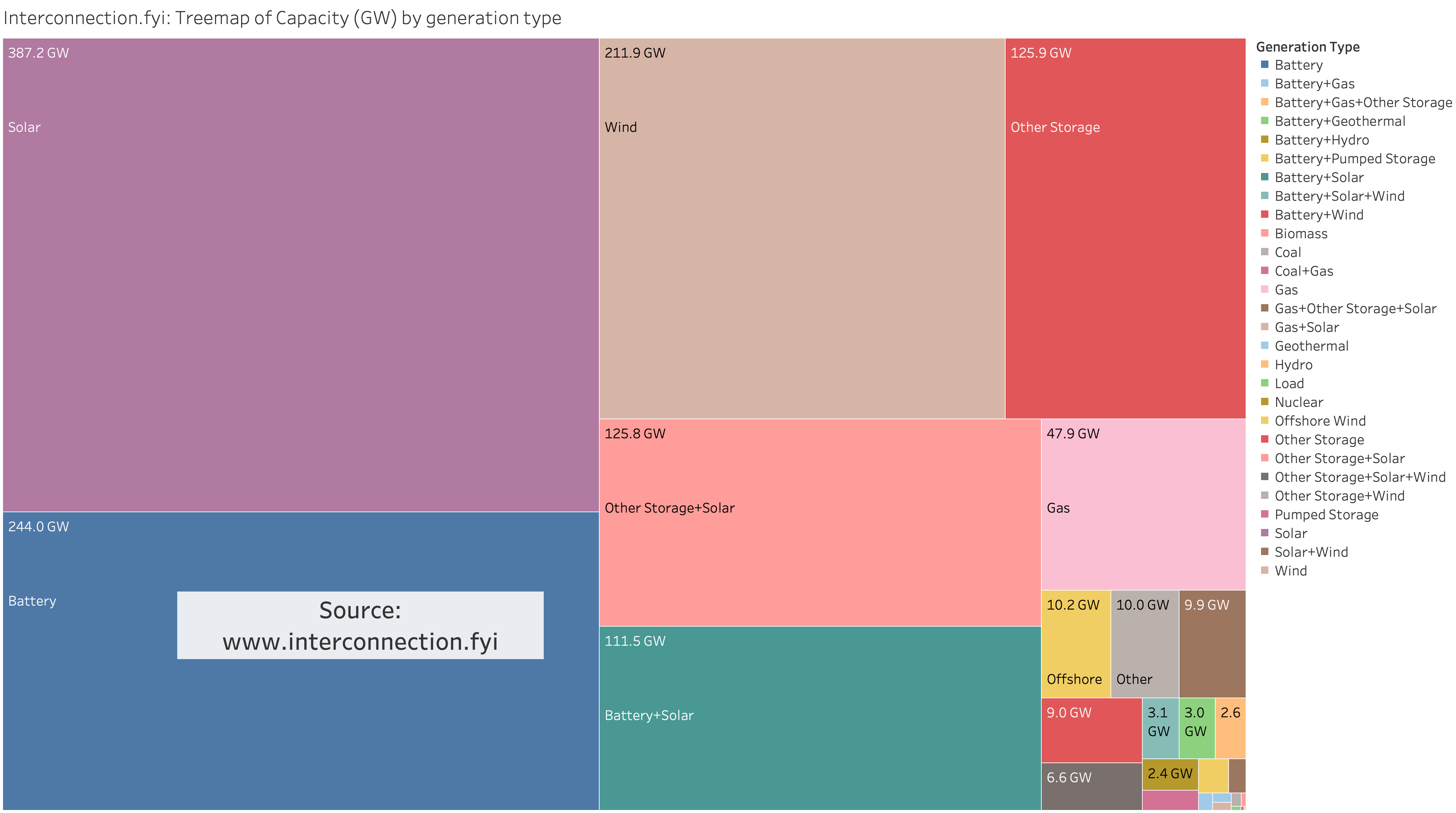

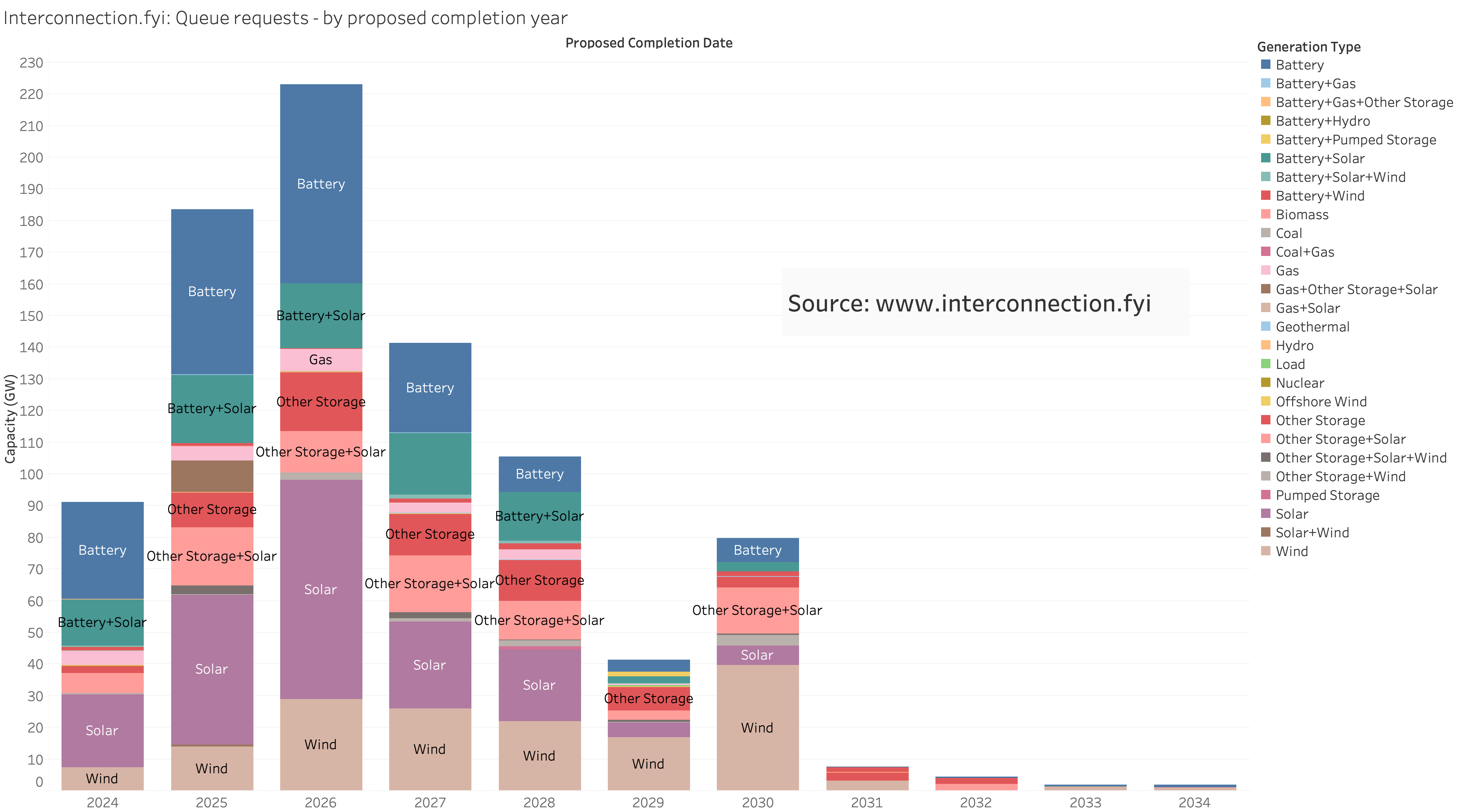

Total capacity by generation type

Standalone solar is the dominant generation type in the queue currently, followed by wind and battery storage. There’s a long-tail of hybrid generation (i.e. solar AND battery storage, or solar AND wind) as well.

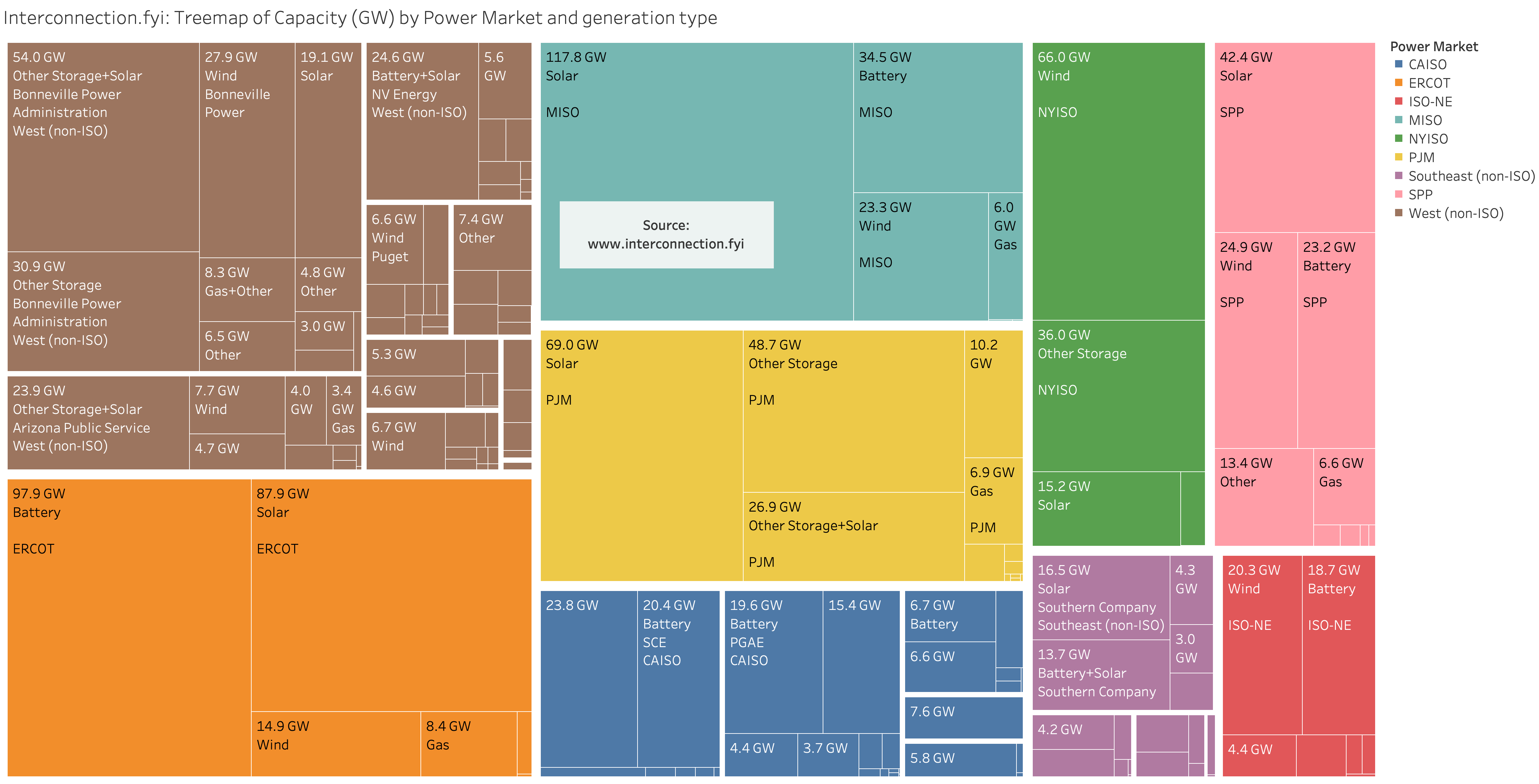

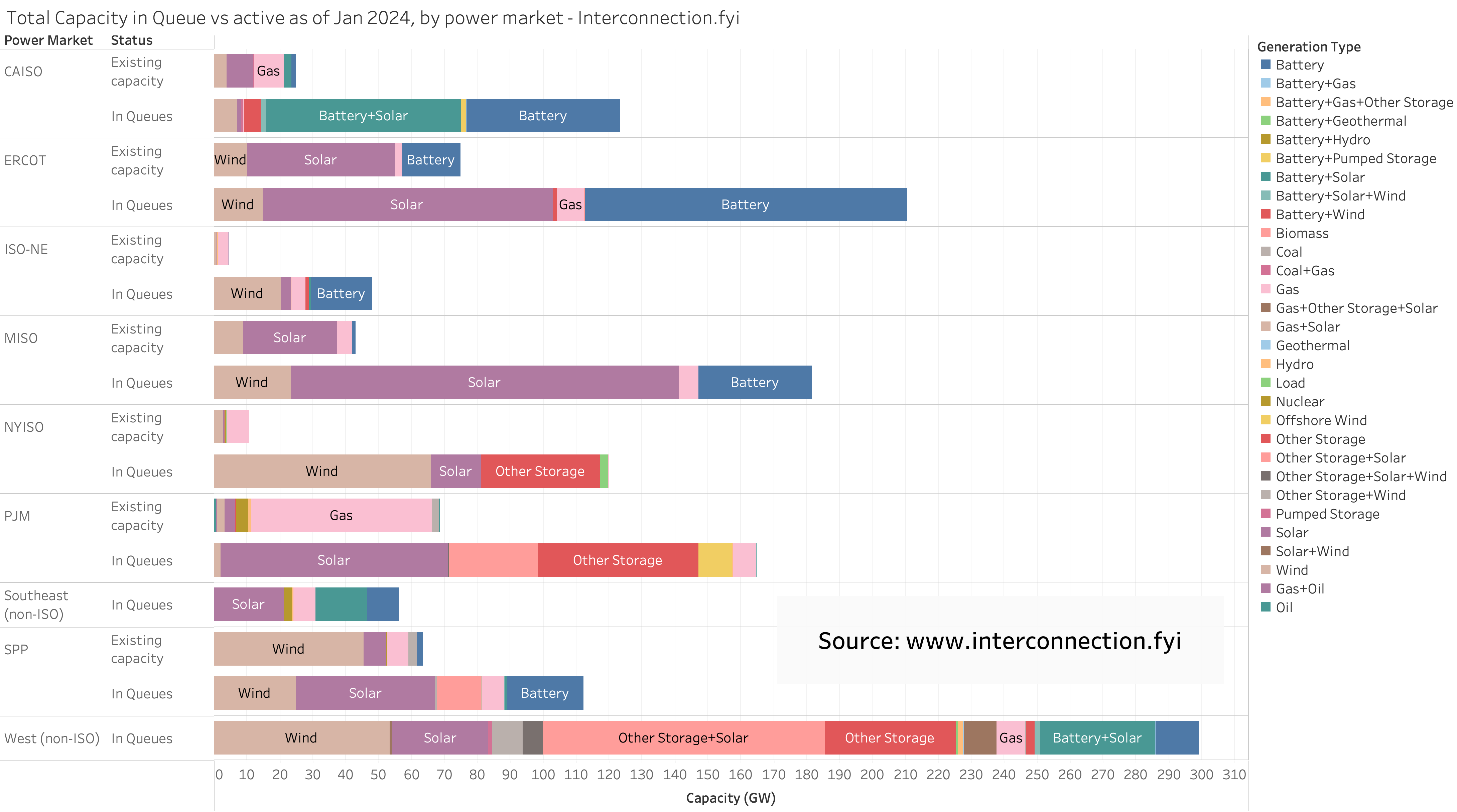

Breaking it down further into each power market:

Total capacity in the queue is higher than existing capacity in many power markets

Note: existing capacity for southeast & west non-ISO is not shown since not all non-ISO utilities publish their in-service/operational queue projects

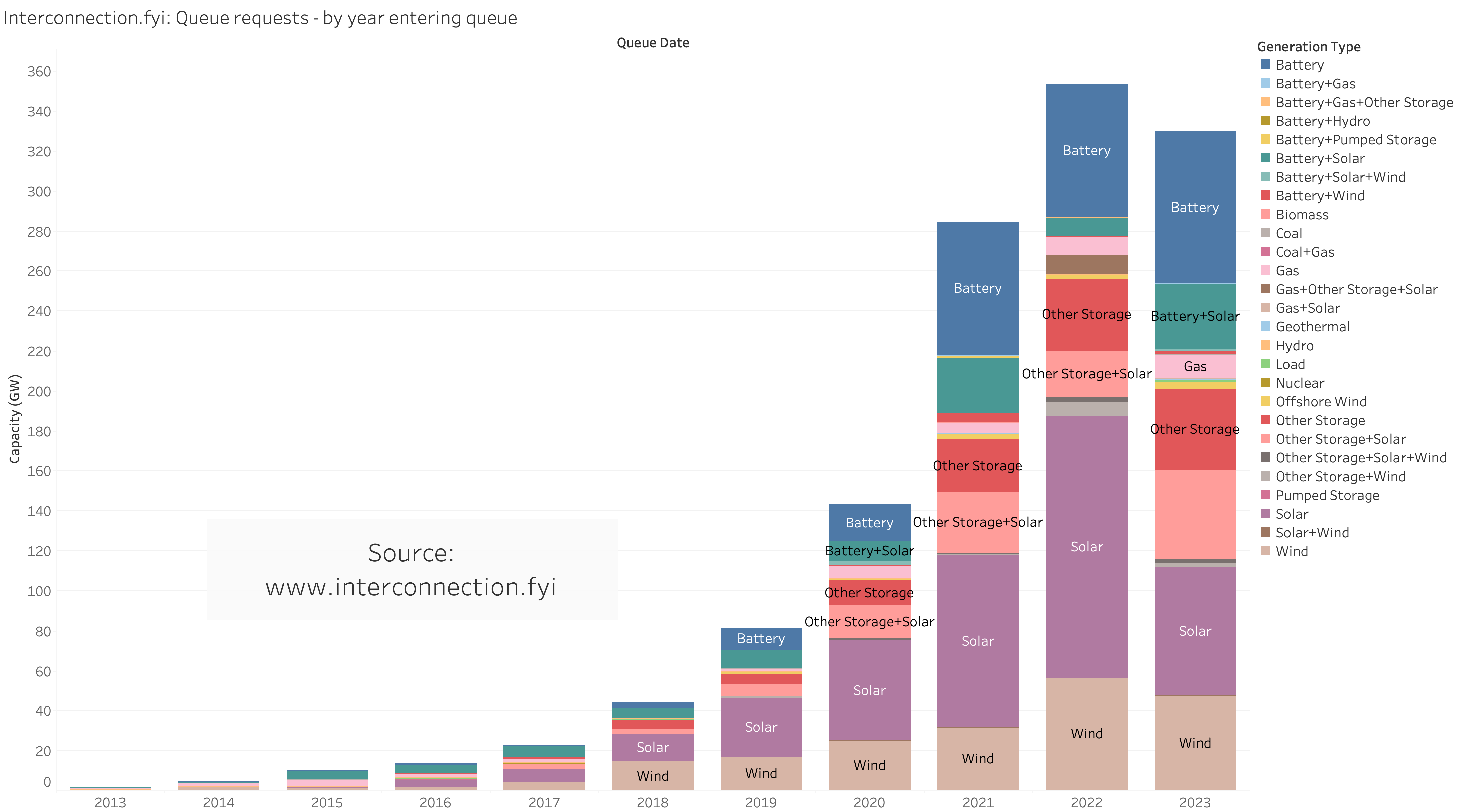

Planned capacity entering the queue in 2023 declined slightly after several years of high growth

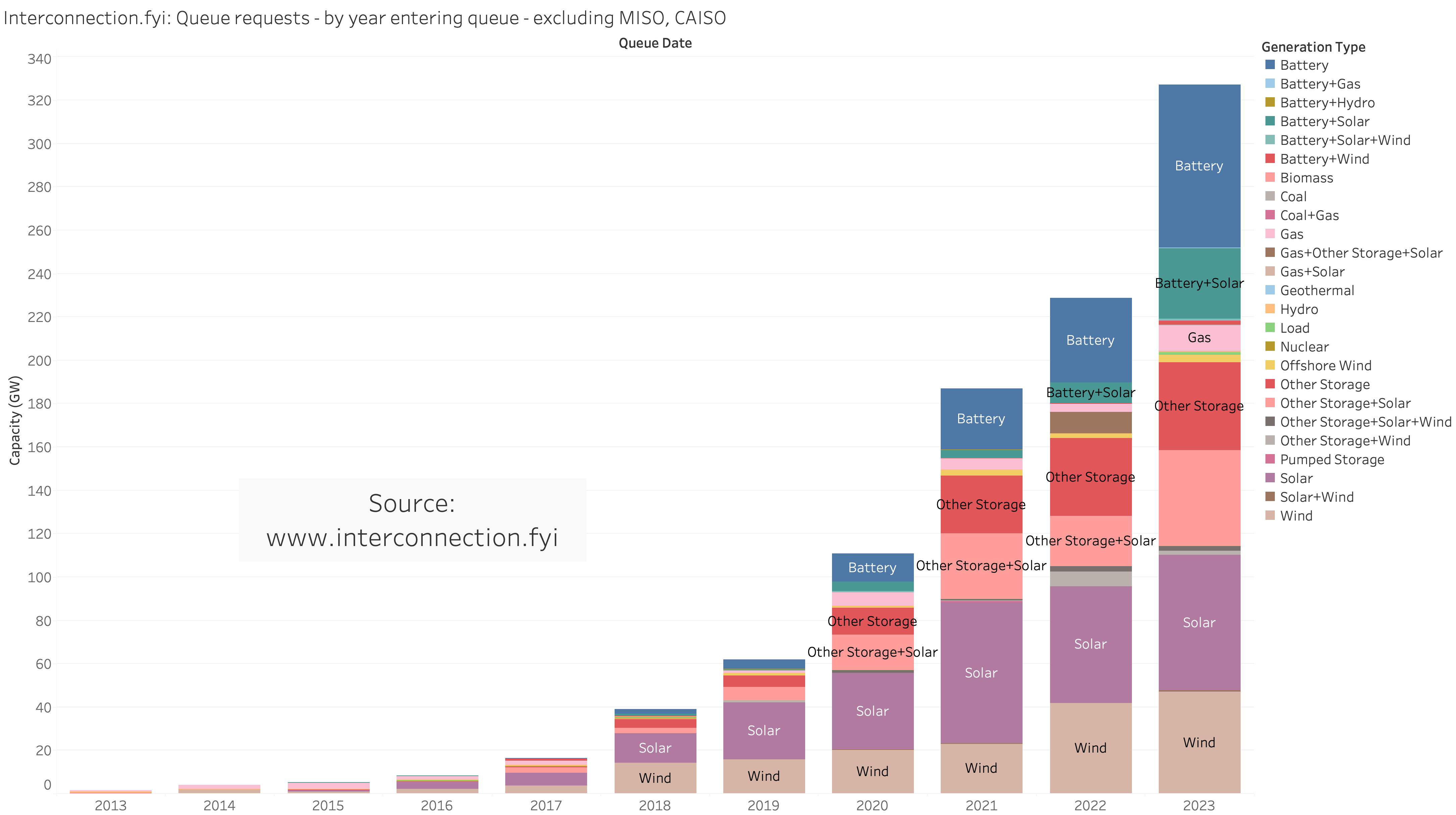

Excluding CAISO and MISO, we still have an upward trend

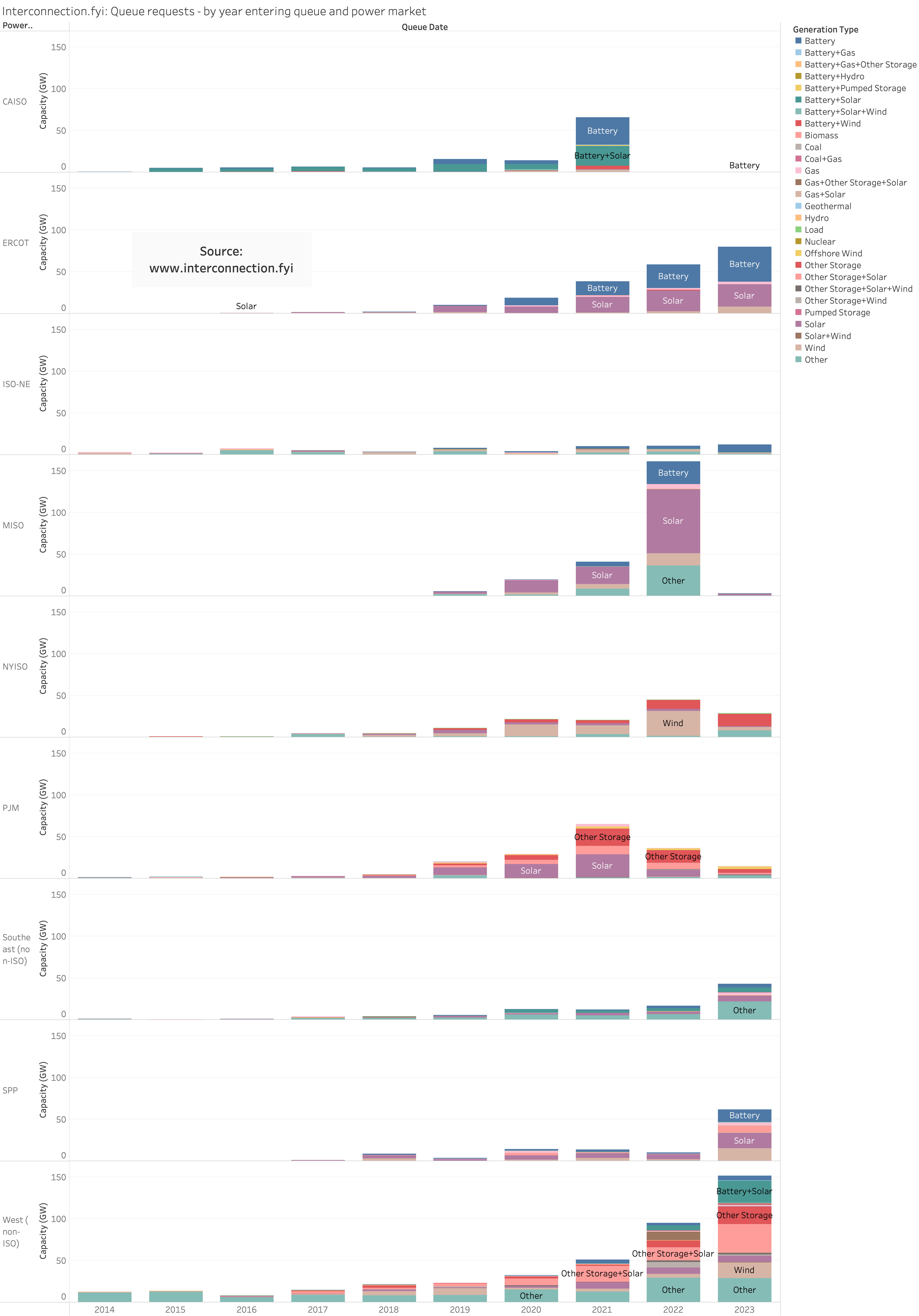

And here’s the same chart broken down by power market , showing how MISO and CAISO have effectively stopped taking new requests in their queues in 2023 and 2022 respectively. Scroll to the bottom of this article to interact with an interactive version of this chart.

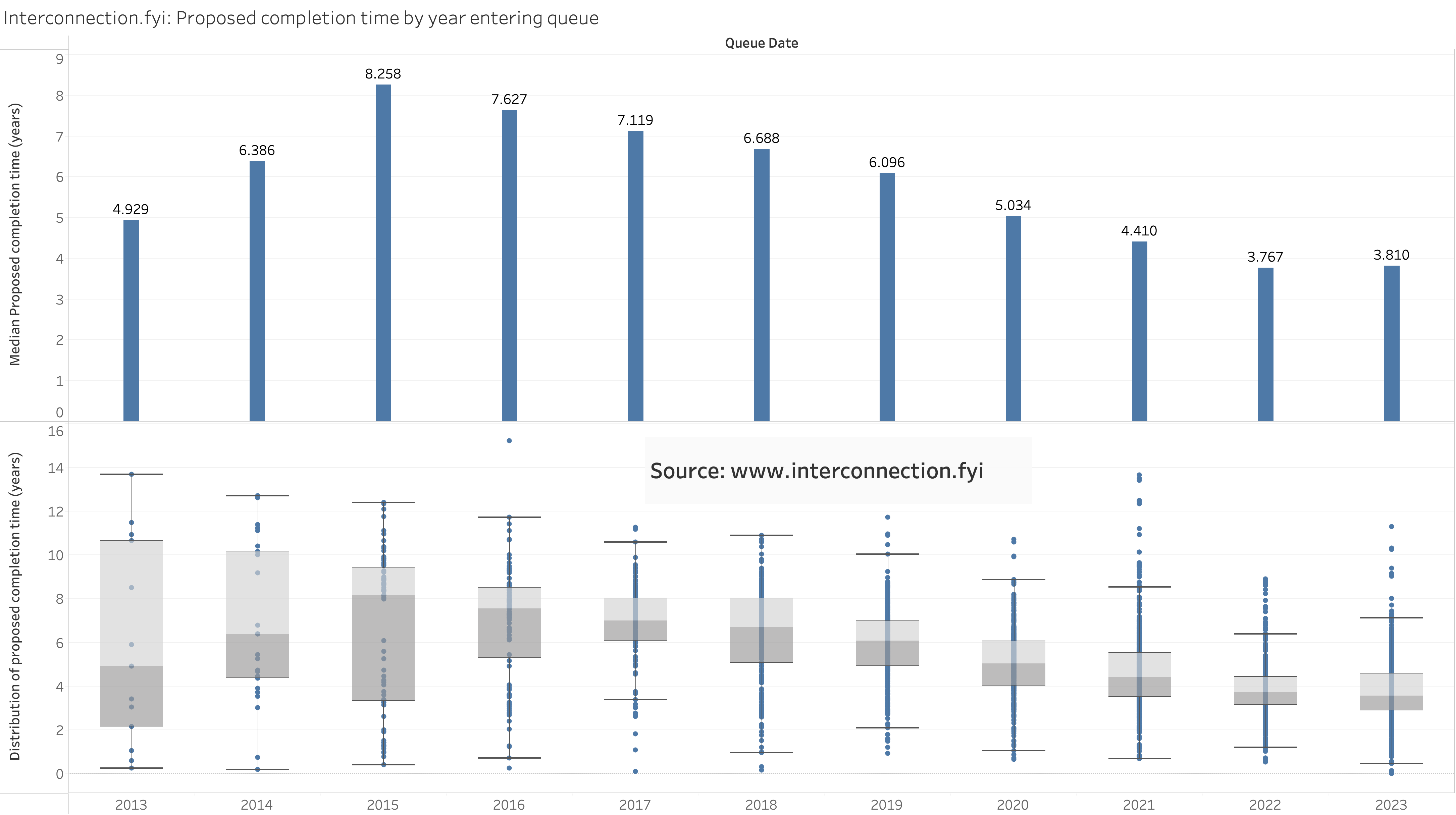

Proposed completion time analysis

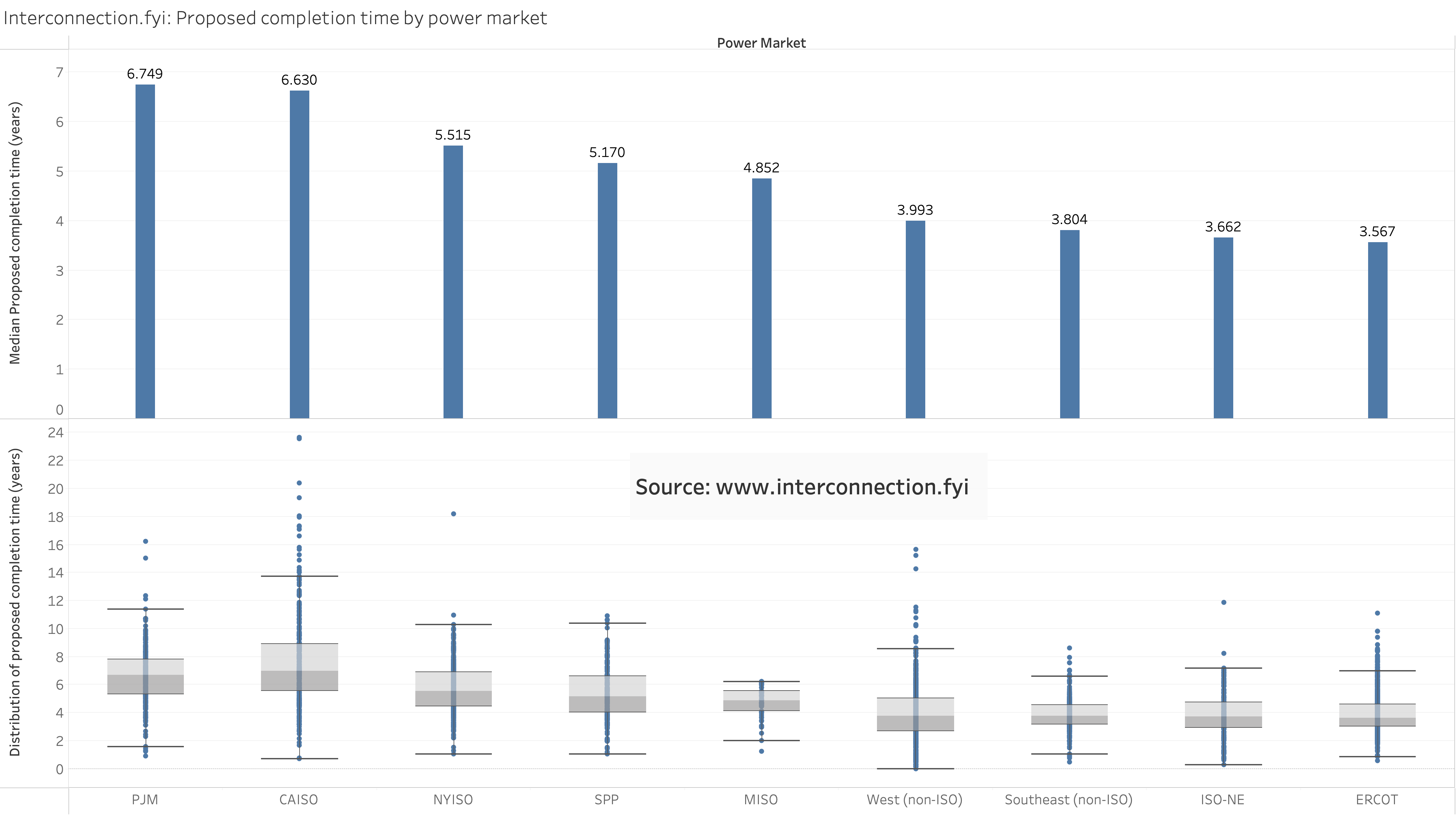

If we take the proposed completion date and subtract it by the enqueued date, we get a proposed completion time

CAISO and PJM have the longest median proposed completion times over all time (CAISO’s spread arguably worse)

Median completion time decreased for projects entering the queue in 2022/2023

The majority of proposed completion times for active requests will happen before 2030

Conclusion

By the way, if you’d like to interact with the data via interactive graphics, checkout the embed below (or here) and the charts in our front page https://interconnection.fyi/

👉 If you’d like to purchase the underlying data from this report or want to run a report on a current or historical dataset, see our various self-data products here or email us here

Addendum

Jesse Jenkins (the renowned energy researcher based at Princeton) asked for a chart plotting projects entering and leaving the queue in the same chart. Here it is!

Interactive visualizations:

Interconnection.fyi

Tracking U.S. ISO & utility interconnection queues

Interconnection queue requests/projects in list format

All transmission grid interconnection queue requests/projects All distribution grid (DG) interconnection queue requests/projects Data center projects by state EIA860 planned and operational power plant projectsInsights

Charts State of interconnection queues — January 2024In 2024, interconnection queues shrank for the first time in yearsAll insightsOther energy & climate tools

Inflation Reduction Act Bill Text Viewer ToolClimate Tech Jobs Tracker (30,000+ jobs)Climate Tech Hiring Trends & ChartsBuy/Sell Surplus TransformersQueue requests/projects by country

Queue requests/projects by power market

CAISO SPP PJM NYISO ERCOT ISO-NE MISO West Southeast AESO IESO Quebec Maritimes BC Manitoba Saskatchewan

Queue requests/projects by status

Active queue requests/projectsWithdrawn queue requests/projectsOperational queue requests/projectsSuspended queue requests/projectsUnknown queue requests/projects

Queue requests/projects by cluster

Queue requests/projects by U.S. state

Queue requests/projects by Canadian province

Data Centers

All data center projectsBy U.S. State

Interconnection queue requests/projects by transmission owner

Alberta Electric System OperatorAllegheny PowerAlliant Energy EastAlliant Energy WestAmeren IllinoisAmeren MissouriAmerican Electric PowerAmerican Municipal PowerAmerican Transmission CompanyAmerican Transmission SystemsArizona Public ServiceArkansas Electric Cooperative CorporationAssociated Electric CooperativeAvista UtilitiesBC HydroBaltimore Gas and ElectricBangor Hydro ElectricBasin Electric Power CooperativeBig Rivers Electric CorporationBlack Hills Cheyenne Light Fuel and Power TransmissionBlack Hills Colorado ElectricBlack Hills PowerBonneville Power AdministrationCedar Falls Municipal Electric UtilityCedar Falls UtilitiesCentral Hudson Gas and ElectricCentral Maine PowerCentral Power Electric CooperativeChelan County Public Utility DistrictCity Utilities of Springfield MissouriCity Water, Light and PowerCity of Columbia, MissouriCity of Muscatine, IowaCleco HoldingsColorado River Storage Project TransmissionColorado Springs UtilitiesCommonwealth EdisonConsolidated EdisonConsumers EnergyCooperative EnergyCorn Belt Power CooperativeDCR TransmissionDairyland Power CooperativeDayton Power and LightDelmarva Power and LightDesertLinkDominion EnergyDominion Energy South CarolinaDuke EnergyDuke Energy CarolinasDuke Energy FloridaDuke Energy IndianaDuke Energy Ohio and KentuckyDuke Energy ProgressDuquesne Light CompanyEast Kentucky Power CooperativeEast River Electric Power CooperativeEast Texas Electric CooperativeEl Paso ElectricEmpire District Electric CompanyEntergyEntergy ArkansasEntergy LouisianaEntergy MississippiEntergy New OrleansEntergy TexasEssential PowerEvergyEvergy Missouri WestEversourceEwington Energy SystemsFarmington Electric Utility SystemFirstEnergyFlorida Power and LightGeorgia TransmissionGrand River Dam AuthorityGrand River EnergyGrant County Public Utility DistrictGridLianceGridLiance WestGridUnityHenderson Municipal Power and LightHoosier EnergyHorizon West TransmissionHydro-QuébecIMEUISO New EnglandITC Great PlainsITC MidwestITC TransmissionIdaho Power CompanyImperial Irrigation DistrictIndependence Power and LightIndependent Electricity System OperatorIndianapolis Power and LightJacksonville Electric AuthorityJersey Central Power and LightKACYKansas City Board of Public UtilitiesKansas City Power and LightKansas Power PoolLS PowerLS Power Grid New YorkLafayette Utilities SystemLea County Electric CooperativeLincoln Electric System

Long Island Power AuthorityLos Angeles Department of Water and PowerLouisville Gas and Electric and Kentucky Utilities EnergyLoveland Area Projects TransmissionLower Yellowstone Rural Electric CooperativeMadison Gas and ElectricMaine Public ServiceManitoba HydroMetropolitan Edison CompanyMichigan Electric Transmission CompanyMichigan Public Power AgencyMid-Kansas Electric CompanyMidAmerican EnergyMidcontinent Independent System OperatorMidwest EnergyMinnesota Municipal Power AgencyMinnesota PowerMinnkota Power CooperativeMissouri River Energy ServicesMissouri Western Energy CorporationMontana-Dakota UtilitiesMunicipal Commission of BoonvilleNAEANB PowerNV EnergyNational GridNavajo-CrystalNebraska Public Power DistrictNew York Power AuthorityNew York State Electric and GasNew York TranscoNextEra Energy TransmissionNextEra Energy Transmission SouthwestNorthWestern EnergyNortheast UtilitiesNorthern Indiana Public ServiceNorthern States Power CompanyNorthwest Iowa Power CooperativeNorthwestern Wisconsin Electric CompanyNova Scotia PowerOhio Valley Electric CorporationOklahoma Gas and ElectricOld Dominion Electric CooperativeOmaha Public Power DistrictOrange and RocklandOrlando Utilities CommissionOtter Tail Power CompanyPECO Energy CompanyPJMPPL CorporationPacifiCorpPacific Gas and Electric CompanyPennsylvania Electric CompanyPeople's Electric CooperativePlatte River Power AuthorityPortland General ElectricPotomac Electric Power CompanyPrairie PowerPublic Service Company Of ColoradoPublic Service Company of New MexicoPublic Service Electric and GasPuget Sound EnergyRochester Gas and ElectricRochester Public UtilitiesRockland Electric CompanySacramento Municipal Utility DistrictSalt River ProjectSam Houston Electric CooperativeSan Diego Gas and ElectricSantee CooperSaskPowerSeminole Electric CooperativeSouth Mississippi Electric Power AssociationSouthern California EdisonSouthern CompanySouthern Illinois Power CooperativeSouthern Indiana Gas and Electric CompanySouthern Maryland Electric CooperativeSouthern Minnesota Municipal Power AgencySouthwestern Power AdministrationSouthwestern Public Service CompanySunflower Electric Power CorporationTacoma Public UtilitiesTampa Electric CompanyTennessee Valley AuthorityTransource MissouriTri-State Generation and Transmission AssociationTucson Electric PowerUnited Gas Improvement CompanyUnited Illuminating CompanyUpper Peninsula Power CompanyValley Electric AssociationVillage of ArcadeWAPA Sierra NevadaWAPA/BEPC/HCPD Integrated SystemWabash Valley Power AssociationWestar EnergyWestern Area Power AdministrationWestern Area Power Administration Desert Southwest RegionWestern Farmers Electric CooperativeWisconsin Electric Power CompanyWisconsin Public Service CorporationWolverine Power Supply CooperativeXcel Energy

Interconnection queue requests/projects by year

Queue requests/projects in 2026Queue requests/projects in 2025Queue requests/projects in 2024Queue requests/projects in 2023Queue requests/projects in 2022Queue requests/projects in 2021Queue requests/projects in 2020Queue requests/projects in 2019Queue requests/projects in 2018Queue requests/projects in 2017Queue requests/projects in 2016Queue requests/projects in 2015Queue requests/projects in 2014Queue requests/projects in 2013Queue requests/projects in 2012Queue requests/projects in 2011Queue requests/projects in 2010Queue requests/projects in 2009Queue requests/projects in 2008Queue requests/projects in 2007Queue requests/projects in 2006Queue requests/projects in 2005Queue requests/projects in 2004Queue requests/projects in 2003Queue requests/projects in 2002Queue requests/projects in 2001Queue requests/projects in 2000Queue requests/projects in 1999Queue requests/projects in 1998Queue requests/projects in 1997Queue requests/projects in 1996Queue requests/projects in 1995© 2026 Interconnection.fyi. All rights reserved.

GridTracker by Interconnection.fyi

Full access to the data

See all the data

Find relevant dockets and filings

Track data center builds